2022/23 market forecast: highly seasonal with a chance of Summer hits

December 8, 2022

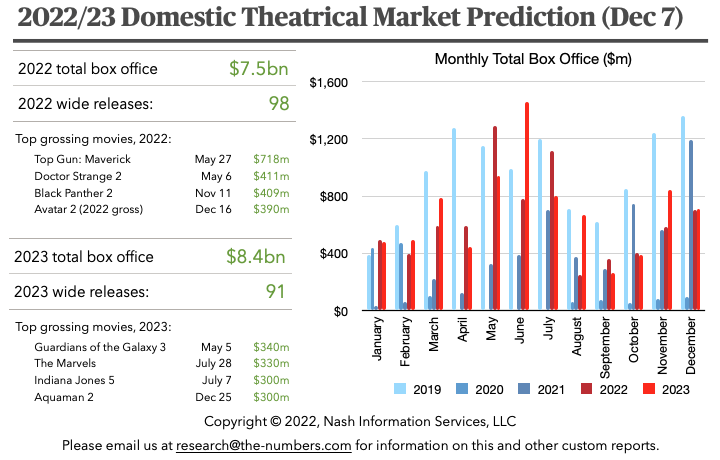

Today we’re publishing our first full-year prediction for 2023, and our final analysis for 2022. The good news is that our model thinks the theatrical market will grow in 2023 by about 10% from this year. The bad news is that it will still fall well short of pre-pandemic numbers, in large part due to a lack of films being released outside of a brief Summer season.

Subscribe to our Bankability and Box Office report for full details, or read on for an overview of what our model thinks of the next 12 months in movie theaters…

Here’s an overview of how everything looks through the rest of this year and in 2023. The bars in the chart estimate the total box office for all films released in a particular month.

Our full-year prediction for 2022 stood at $7.4 billion this time last month, so it’s up a little bit this time around. That’s entirely due to a methodological change though. We’re now calculating the money earned during a calendar year, rather than the amount earned by films released during a year. That means the $241 million earned by Spider-Man: No Way Home since January 1 of this year now counts towards 2022’s total. Without that, our prediction for 2022 would have declined somewhat.

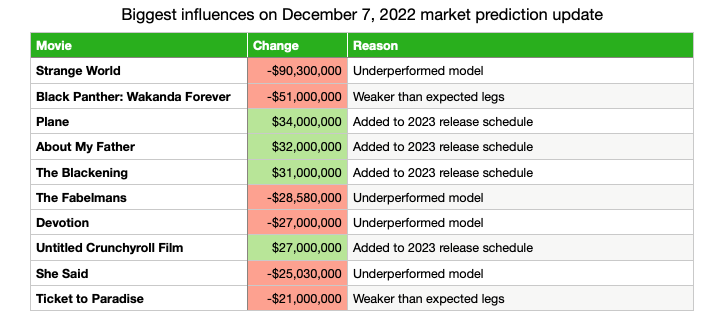

This chart explains why:

Disney’s Thanksgiving release, Strange World, performed dramatically worse than expected. In fact, it looks as though it will be the worst-performing major studio release of the year when compared to what the model thought it should do. It’s currently expected to earn just 17% of the model’s original prediction. The Fabelmans is performing almost as badly, as it is currently tracking towards earning just 19% of what the model thought it should. Add to that underperformances from She Said, Bones and All, and Devotion, and we’re looking at a very disappointing start to the Holiday Season.

On top of that, Black Panther: Wakanda Forever and Ticket to Paradise have both had slightly worse than expected legs through Thanksgiving and into the first part of December. Neither film is performing badly overall, but they both looked as though they might have great runs, and that hasn’t quite panned out.

All of those disappointing numbers almost completely counteract the positive technical effect of including films that played into the New Year of 2022 in the market estimate. We will still end the year with a market about 50% bigger than 2021 as a whole, but possibly not growing very much at the moment.

Our first prediction for the whole of 2023 is for $8.4 billion in total spending. Like this year, it looks as though that will be heavily concentrated into a period that lasts just three months from the beginning of May to the end of July. The model is particularly confident about the prospects for Guardians of the Galaxy Vol. 3, Indiana Jones and the Dial of Destiny, and The Marvels; but we will have another streak of nine weeks with a potential $100-million movie coming out virtually every weekend—other eyecatchers are Fast X, The Little Mermaid, Spider-Man: Across the Spider-Verse, Transformers: Rise of the Beasts, Elemental, The Flash, Mission: Impossible, Dead Reckoning—Part One, Barbie and Oppenheimer.

Once the Summer purple patch is over, we’re looking at another dramatic slowdown in movies likely to generate much business. In fact, September and October look as though they could be even slower than they were this year. Fortunately, Dune: Part 2 and The Hunger Games: The Ballad of Songbirds and Snakes will at least give the Holiday Season a chance of starting strongly, and Aquaman and the Lost Kingdom could have a great Christmas. We could do with a few more releases in December though, and I’ll be surprised if something doesn’t show up in that slot as new release dates are announced over the next month or two.

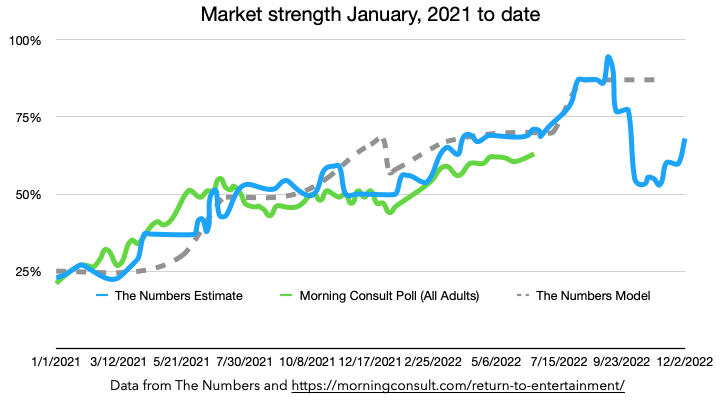

The problems caused for the industry by these big “dead spots” in the release calendar show up in our week-to-week estimate of overall market strength. After nearly recovering completely during the Summer rush earlier this year, our model’s estimate of the strength of the market compared to pre-pandemic levels fell from over 90% to a shade over 50% during September and October. It has picked up a little now, and I think the underlying market potential is around 80% to 90% of pre-pandemic levels, but it looks as though the studios will need to pick up their game outside of the Summer if we’re going to sustain a year-round market recovery. For now, the prediction for 2023 is based on an assumption that the market will recover to 90% of its pre-pandemic level over time, but that’s something I’ll be lookin at more closely in the New Year.

Now we have a full set of predictions for 2023, we have one new movie that it looking like a potential breakout hit based on current audience interest. Wonka, starring Timothée Chalamet, is currently getting an unusual level of interest given it’s 12 months out. It joins Oppenheimer and Barbie as films that model isn’t enthusiastic about, but for which audiences are showing strong interest.

For full details of which movies our audience tracking suggests will have breakout performances, a list of predictions for all movies coming out in wide release between now and the end of 2023, plus the latest updates to our Bankability values for acting and creative talent in the industry, purchase or subscribe to our Bankability and Box Office report.

Our market prediction is based on the same model as the weekend predictions that we’ve been running since theaters started reopening towards the end of 2020. We are now running the prediction model for every announced wide release on the release schedule and estimating the size of the market as a whole by assuming a relatively small amount of additional revenue from limited releases. The prediction for each movie is based on six factors:

The performance of similar films in recent years, and cast and crew Bankability. So far as possible, the model uses films in the same genre released by the same distributor as points of comparison. The predicted performance of franchise films is based on previous releases in the franchise. Cast and crew Bankability is weighted more heavily for non-franchise than for franchise films.

The current state of the theatrical market. We update our model after each weekend with a wide release to estimate what proportion of formerly-regular moviegoers are currently going to theaters.

Adjustments for specific genres. The pandemic has affected different segments of the audience in different ways. We are currently adjusting movies with romantic content down by 20%, but not adjusting any other genres.

Adjustments for day-and-date streaming releases. This was taken into account when films were being simultaneously released on HBO Max and in theaters on the same day. Since that’s no longer happening, and we haven’t seen a measurable impact from films being released simultaneously on Peacock and Paramount+, no adjustment is currently being made. We are continuing to monitor this aspect of the industry.

Potential breakout hits. Films that have the potential to break out beyond what the model otherwise predicts are identified and their predictions increased accordingly. These films are currently selected based on our measurement of audience interest.

The expected recovery of the theatrical market as the pandemic is brought under control. The model assumes that the market will settle back to 90% of its pre-pandemic size at the end of the recovery. Growth was slow at first, accelerated as more people become confident in going to theaters, and then will slow down as more cautious moviegoers take time to return to attending. This is the classic ''S-shaped'' curve seen in economics textbooks (and in many cases in the real world). (For more on this see my previous article, How quickly can the box office recover?) The model assumes that this recovery started on April 1, 2021, plateaued in July due to the wave in COVID in infections caused by the Delta variant, and started again when cases waned at the beginning of October. The rise of the Omicron variant at the beginning of 2022 caused another slowdown. Those parameters are likely to be adjusted as the market situation evolves.

- Current release schedule

Bruce Nash, bruce.nash@the-numbers.com

-1-News.jpg)

Methodology

- Recent release schedule changes

- Subscribe to the Bankability Index for full details on our market predictions

Filed under: Timothée Chalamet