Our 2021 forecast: how the box office might recover

April 1, 2021

Warner Bros. reported a $9.6-million opening day for Godzilla vs. Kong this morning, the best single day at the box office since Onward’s opening weekend back in March last year. Coupled with bigger-than-expected debut outings for Tom and Jerry and Nobody, the signs point towards a growing domestic theatrical market as theaters open up, people get vaccinated, and (fingers crossed) the US and Canada emerge from the worst of the COVID-19 pandemic.

I’ll have more to say on Godzilla vs. Kong’s opening in tomorrow’s weekend prediction column, but today I’m pleased to introduce our long-range box office forecast. This extends our weekend prediction model to all films currently on the release schedule through the end of 2021, and also predicts how much each film will make in total. Each month, I’ll provide a monthly snapshot here on The Numbers, and full details will be in our monthly Bankability Report, available by subscription.

Without further ado, here’s what the model says today for the market prospects for 2021.

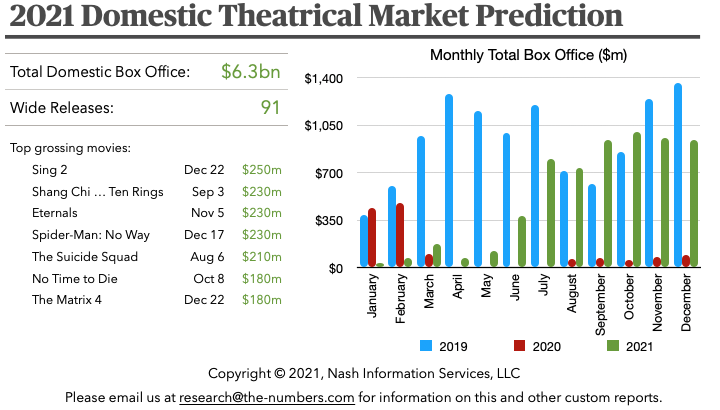

Our model is currently predicting a total box office of $6.3 billion in the domestic (United States and Canada) theatrical market in 2021. Unsurprisingly, the vast majority of that income is expected to come in the later part of the year, and all of the top-grossing films are expected to be released between August and December.

Right now, there’s something of a traffic jam of big films scheduled to come out between August and October, and the model thinks that those months could see higher box office than the equivalent months in 2019. That run begins with Shang Chi and the Legend of the Ten Rings, and includes Venom: Let There Be Carnage, Dune, and No Time to Die. Can the market sustain that many big releases during what is usually a slower season at the box office? Or will we see some more shuffling from the studios as the pace of the box office recovery becomes clear? I suspect the latter.

After that burst of activity, things look likely to slow down in November and December compared to previous years. That’s mainly because there isn’t a film on the release slate that looks like a sure-fire mega blockbuster on the scale of 2019’s Frozen II and Star Wars: The Rise of Skywalker. Of course, one of the films on the release schedule could break out to those kind of numbers—that’s one of the reasons it’s fun to follow the box office results—but our model doesn’t see an individual film that’s virtually bound to do so.

However things turn out, we’ll publish an update to this forecast each month and keep track of how our model’s prediction is changing as schedules evolve and we see how current releases are doing.

The market prediction is based on the same model as the weekend predictions that we’ve been running since theaters started reopening towards the end of last year. We are now running the prediction model for every announced wide release on the release schedule (plus assuming a relatively small amount of additional revenue from limited releases). The prediction for each movie is based on three factors:

The performance of similar films in recent years, and cast and crew Bankability. So far as possible, the model uses films in the same genre released by the same distributor as points of comparison. The predicted performance of franchise films is based on previous releases in the franchise. Cast and crew Bankability is weighted more heavily for non-franchise than for franchise films.

The current state of the theatrical market. The model assumes there will be no measurable recovery in the theatrical market until the number of COVID-19 cases falls substantially. As of today, it assumes recovery will start today, April 1, thanks to a reduced case count and an increasing number of people who have received a vaccine. This date may be revised as conditions evolve.

The expected recovery of the theatrical market as the pandemic is brought under control. Once the market starts to recover, the model assumes it will take six months to reach a “new normal.” Growth towards the new normal will be slow at first, accelerate as more people become confident in going to theaters, and then slow down as more cautious moviegoers take time to return to attending. This is the classic ''S-shaped'' curve seen in economics textbooks (and in many cases in the real world). The model assumes that the market will settle back to 70% of its pre-pandemic size at the end of the recovery. (For more on this see my previous article, How quickly can the box office recover?)

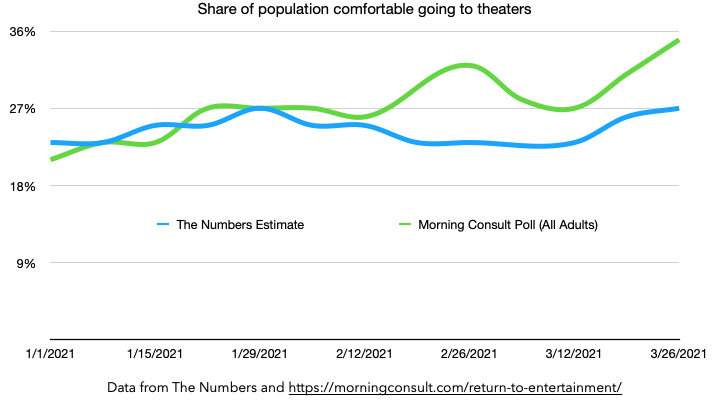

The key metric for making box office predictions right now (what I’ve been calling our “pandemic adjustment”), is the share of the population comfortable with going to movie theaters right now. Regular readers will be familiar with our process of updating this number based on the performance of new releases each week. An alternative way to come up with this figure is to actually ask people, something that Morning Consult have been doing each week since the pandemic lockdowns began. Their excellent tracking page has all the details, and I’ve charted how our figure based on box office results compares with their poll numbers.

Given that our numbers come from completely independent methodologies, it’s reassuring to see them match quite closely. The Morning Consult poll figure has been increasing fairly steadily in the last few weeks, and is now a bit ahead of ours. Hopefully that points towards a growing enthusiasm that our model hasn’t quite caught up with yet. If we only looked at films released in March, our model would estimate that 42% of moviegoers are now comfortable with going to theaters. That’s even higher than Morning Consult’s poll indicates. The reason our pandemic adjustment hasn’t hit that mark yet is down to our model being quite conservative about reading anything into the performance of a single film.

Hopefully by this time next month, we’ll have a clearer picture of the trends, and some more clarity on studios’ release plans. For now, our model thinks there’s grounds for some cautious optimism about the domestic theatrical market.

- Current release schedule

Bruce Nash, bruce.nash@the-numbers.com

-1-News.jpg)

- Recent release schedule changes

- Subscribe to the Bankability Index for full details on our market predictions

Filed under: Monthly Preview