2021 forecast update: market prospects remain steady in spite of shuffled schedules

May 12, 2021

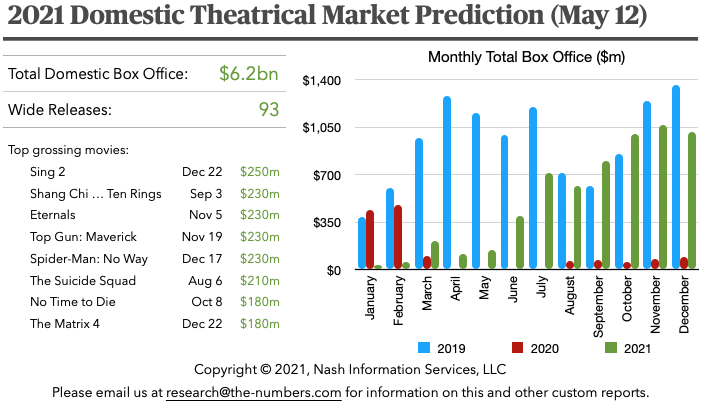

After a month of strong performances at the box office, rearrangements of the theatrical release schedule, and increased vaccinations and slowly falling coronavirus case counts, our 2021 market forecast finds itself just about back where we started. When we introduced our market prediction last month, it looked as though 2021 would end with a total box office gross of $6.3 billion in North America. Today’s update very slightly decreases that number to $6.2 billion.

Each month, we’ll provide a monthly snapshot here on The Numbers, and full details will be in our monthly Bankability Report, available by subscription.

Here’s what the model says today for the market prospects for 2021.

The green bars in the chart above show the expected box office by month in 2021, compared to the red bars for the pandemic-ravaged 2020 box office, and 2019 in blue, which was a relatively normal year. The current release schedule suggests a slight ramp-up in business from May to June, with an almost-normal market in August and more business than usual in September and October due to the major films that are slated to come out much later in the Summer than usual: The Suicide Squad in August, Shang Chi and the Legend of the Ten Rings in September, and No Time to Die in October.

After that rush, the release slate looks more normal in November and December, at least in terms of the type of movie coming out, and the fundamental question turns to whether the market will have fully recovered by then, or if there’s a segment of the population who are either still not convinced of the safety of going to a movie theater, or have become so used to watching major films at home that they’ve lost the habit of going to see films in a theater.

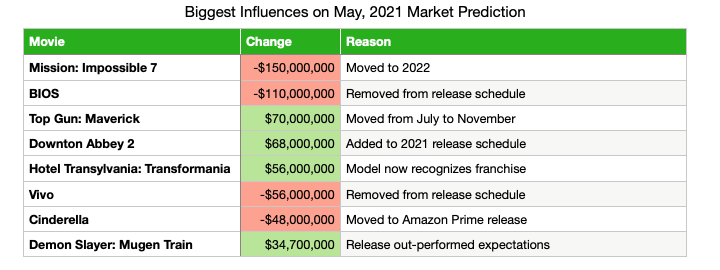

Even though there hasn’t been a huge change from last month in that $6.2-billion top-line number, there have been some announcements that have a major effect individually. On balance, they nearly perfectly cancelled themselves out:

The biggest news in the last month, according to the model, is Paramount’s decision to move two Tom Cruise films, with Top Gun: Maverick moving to November and Mission: Impossible 7 being bumped to May, 2022. While that significantly improves the prospects for Top Gun, since the market is expected to be stronger in November, the loss of Mission: Impossible 7 is the biggest blow to the box office amongst all the changes. Although BIOS wasn’t getting nearly the buzz of either of those films, its pedigree made it a likely solid performer, so the cancellation of its theatrical release is also a significant blow.

On the brighter side, Downton Abbey 2 now has a Christmas release date, and should deliver good business, and Demon Slayer outpaced expectations so much that it boosts the annual projection by over $30 million all on its own. Hopefully the results from some films released in May will help further improve the numbers.

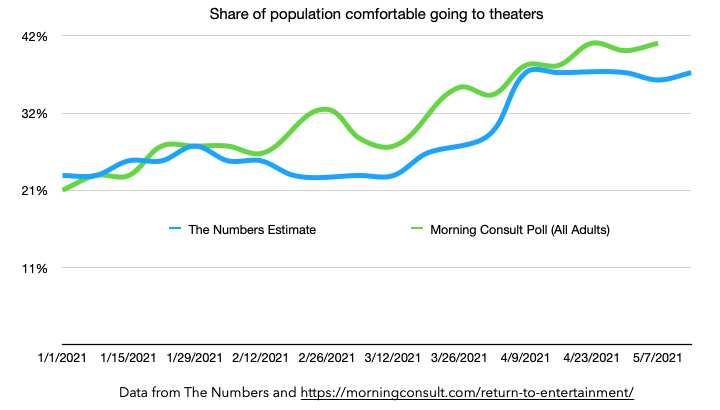

Overall, the market does seem to be recovering, partly because more theaters are opening, but mainly because more people are willing to go to them. Morning Consult’s weekly opinion survey is a good measure of that, and its measurement of returning moviegoers is now over 40% of the population. Our model’s estimate of regular moviegoers going to theaters stalled out a bit in April and early May, and currently sits at 37%. Our numbers and Morning Consult’s continue to track each other closely (click on the chart to go to Morning Consult’s page with more details on their survey):

Our market prediction is based on the same model as the weekend predictions that we’ve been running since theaters started reopening towards the end of last year. We are now running the prediction model for every announced wide release on the release schedule (and assuming a relatively small amount of additional revenue from limited releases). The prediction for each movie is based on three factors:

The performance of similar films in recent years, and cast and crew Bankability. So far as possible, the model uses films in the same genre released by the same distributor as points of comparison. The predicted performance of franchise films is based on previous releases in the franchise. Cast and crew Bankability is weighted more heavily for non-franchise than for franchise films.

The current state of the theatrical market. We update our model after each weekend with a wide release to estimate what proportion of formerly-regular moviegoers are currently going to theaters. As of today, that figure is 37%. We also monitor Morning Consult’s weekly survey of moviegoers, and may make adjustments to our analysis if our number varies significantly from theirs.

The expected recovery of the theatrical market as the pandemic is brought under control. Once the market starts to recover, the model assumes it will take six months to reach a “new normal.” Growth towards the new normal will be slow at first, accelerate as more people become confident in going to theaters, and then slow down as more cautious moviegoers take time to return to attending. This is the classic ''S-shaped'' curve seen in economics textbooks (and in many cases in the real world). The model assumes that the market will settle back to 70% of its pre-pandemic size at the end of the recovery. (For more on this see my previous article, How quickly can the box office recover?) The model assumes that this recovery started on April 1, and will take until the beginning of October. Those parameters might be adjusted as the market situation evolves.

- Current release schedule

Bruce Nash, bruce.nash@the-numbers.com

-1-News.jpg)

Methodology

- Recent release schedule changes

- Subscribe to the Bankability Index for full details on our market predictions

Filed under: Tom Cruise